The ‘retail apocalypse’ is a myth, and that's good news for the shopping industry and downtowns

This is one of a series of ongoing Public Square articles on the market, technological, and cultural transformation of the $5 trillion retail industry—and how it relates to a continued shift toward walkable, urban living.

It is essential to debunk the myth of the “retail apocalypse” and change the dialogue about the future of retail nationwide, in our downtowns, and all urban settings. By challenging mainstream media and shifting the conversation, new faith and encouragement can be instilled for many of our colleagues across many overlapping professions.

Confidence is warranted in the retail industry for urban and town planners, municipal planning staff, planning commissioners, commercial real estate brokers, developers, and investors. Continuing to plan, design, approve, and build retail space for merchants in urban settings and mixed-use projects makes sense. Downtown building owners and downtown managers can stay focused on filling vacancies with traditional merchants and restaurants, rather than leasing to non-retail services or the first taker.

Also, downtown managers can use this article's data to present a more realistic view to their existing and prospective merchants. In a future article, I will arm merchants with tools and best practices for taking back a share of the market and thriving—even while sprawling regional malls continue to contract and outdated chain stores retreat.

The “retail apocalypse” is a concept being actively promoted through media headlines, and it is largely based on recent closures among national chain stores. However, it is easily debunked with real data. The total number of retail establishments and aggregate retail sales are actually increasing, and new chain stores and restaurant openings are keeping up with chain store closures.

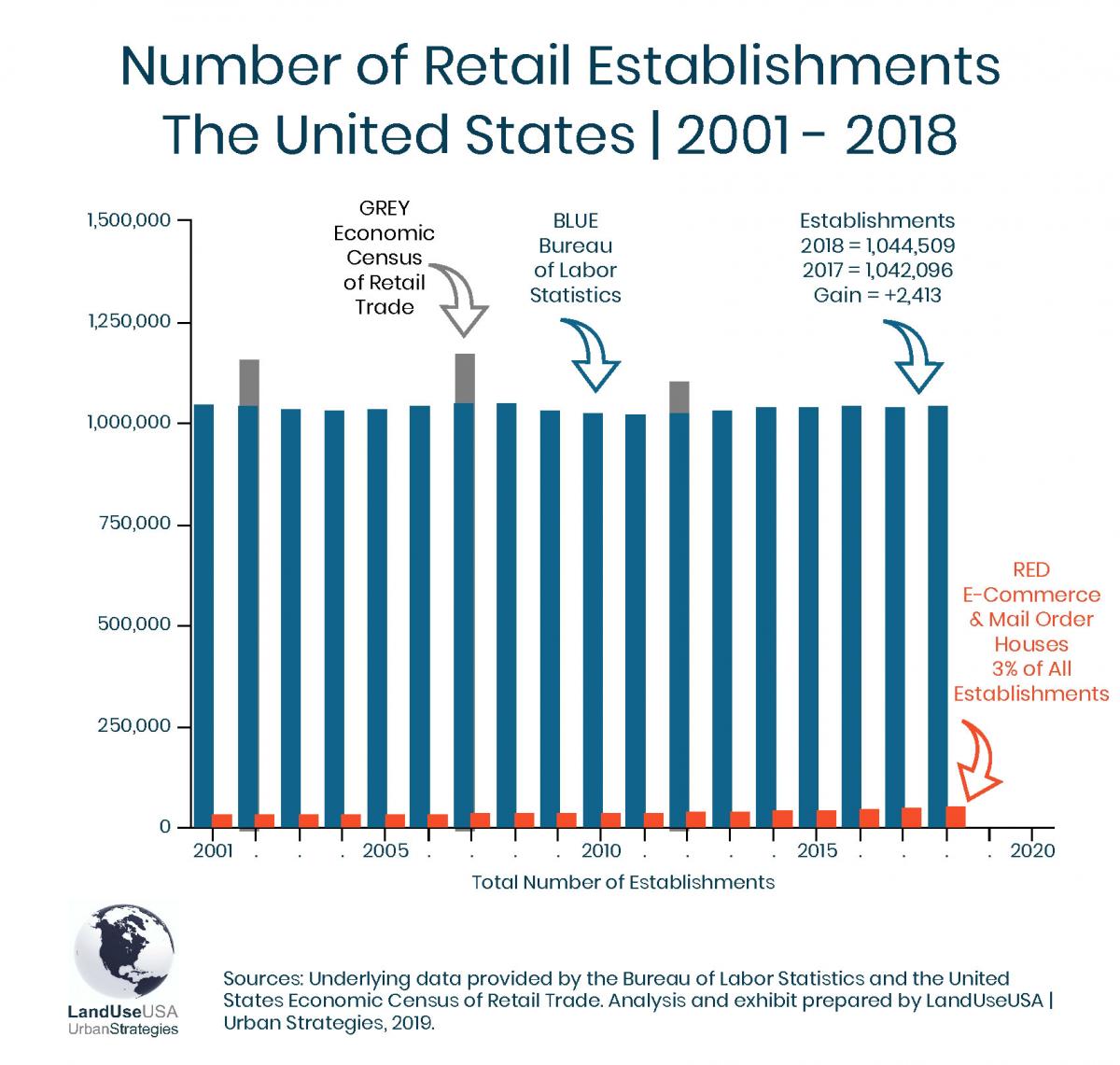

Increasing retail establishments: The hypothetical Retail Apocalypse should be supported by a decline in the total retail establishments, but that's not the case. The Bureau of Labor Statistics (BLS) reported 1,044,509 establishments for 2018, for a net gain of 2,413 establishments over 2017 (1,042,096). The 2018 figure also represents a net gain of more than 20,800 establishments since a retail trough in 2011, a low point resulting from the Great Recession.

A timeline of total retail establishments since 2001 is shown in Figure 1. This same chart also shows a timeline of e-commerce establishments and mail order houses (i.e., non-stores). They currently total 33,000 and represent just 3 percent of all retail establishments.

New stores offset the closings: The growth of retail trade can be tough to imagine given all of the announcements of store closings across the nation, and particularly with media channels fanning the flames. Chain store closings get inflated coverage because it helps sell news channels. With that primary objective, reporters too quickly ignore new store and restaurant openings that offset the closures.

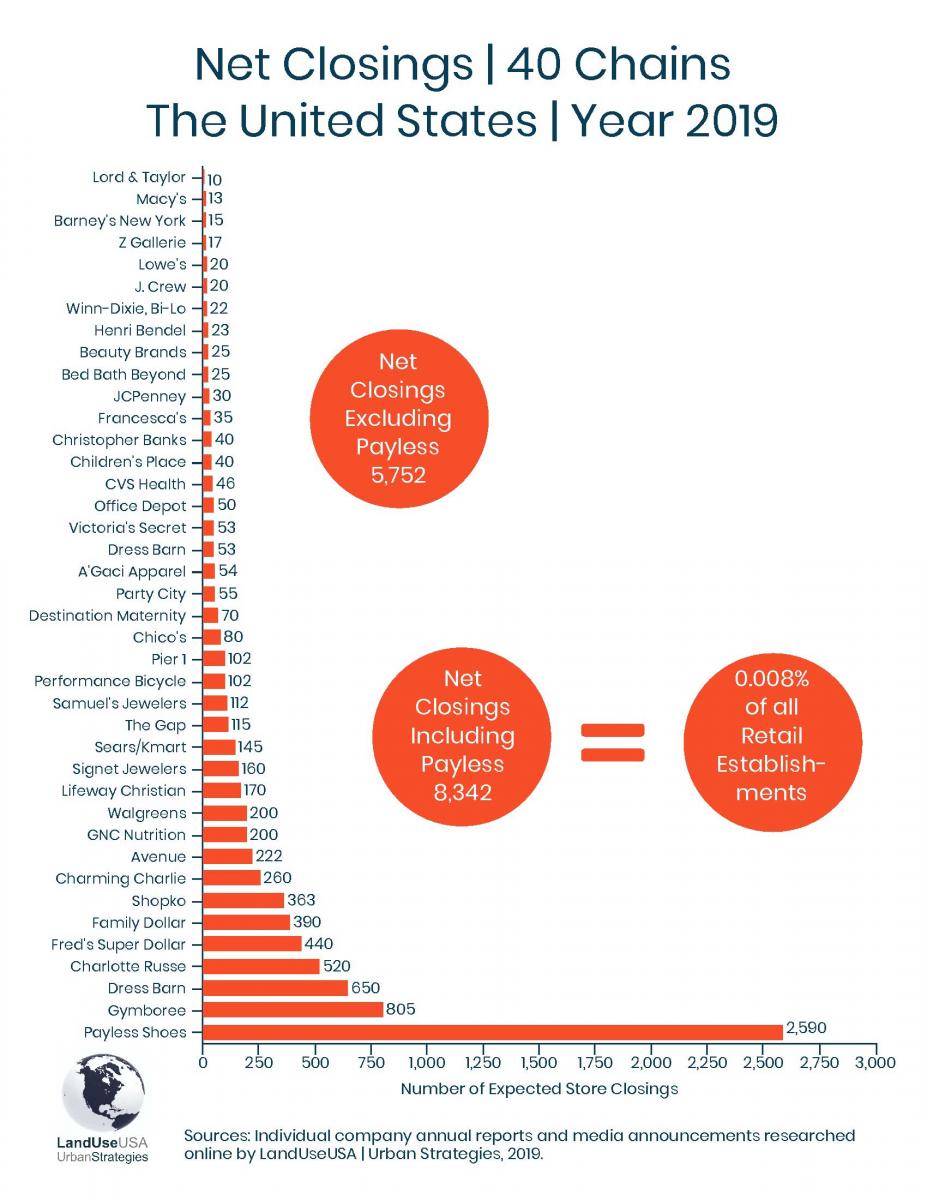

To further debunk the myth of a Retail Apocalypse, LandUseUSA conducted an in-depth survey of announced chain store closings and openings, and assembled the findings in figures 2 and 3. The inventory includes the top 40 largest chain store closures and the top 40 largest chain store openings. Based on these inventories, at least 8,342 chain store locations will close in 2019, including 2,590 Payless shoe stores. Others are in the hundreds and include Gymboree (-805), Dress Barn (-650), Charlotte Russe (-520), Fred’s Super Dollar (-440), Family Dollar (-390), Shopko (-363), Sears/Kmart (-145) and the Gap (-115).

Here are some more facts to put this in context. First, the top 40 chain store closures represent a mere 0.8% of all retail establishments reported in 2018. That is 8 stores out of every one thousand (8/1,000); and the other 99.2% of all retail establishments (992 out of every thousand) are actually growing in total numbers.

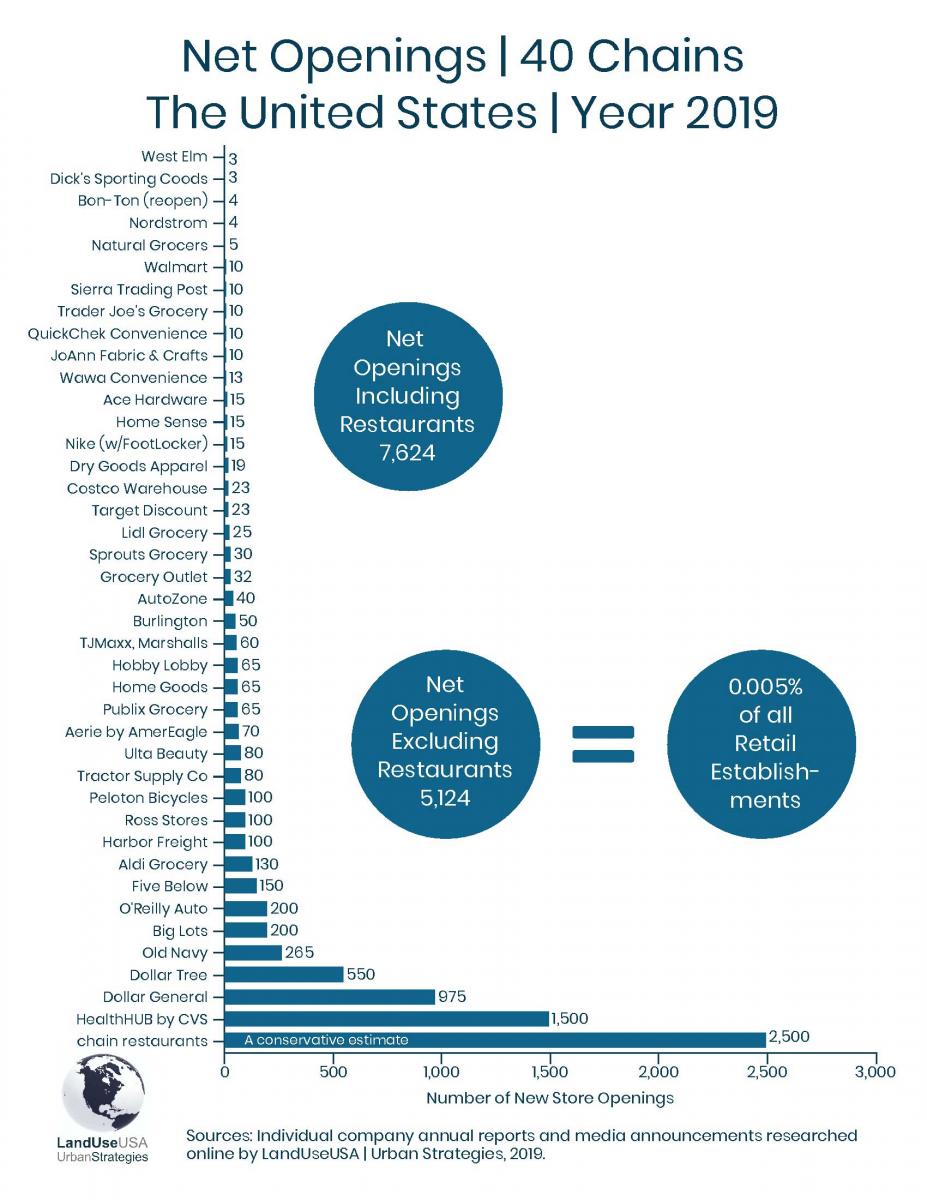

Furthermore, the nation’s new chain store openings will total at least 5,124 in 2019 (0.5%). There are also 2,500 net new restaurants opening in 2019 (this is a conservative estimate), which helps make up any remaining gap between store openings versus closings.

It is also worth noting that the Payless shoe store closings represent more than 30 percent of the top 40 chain store closures. If Payless Shoes is removed from the count, then all other losses are nearly offset by new store openings. If the new restaurants (2,500) are added to the mix, then there is a net gain rather than loss.

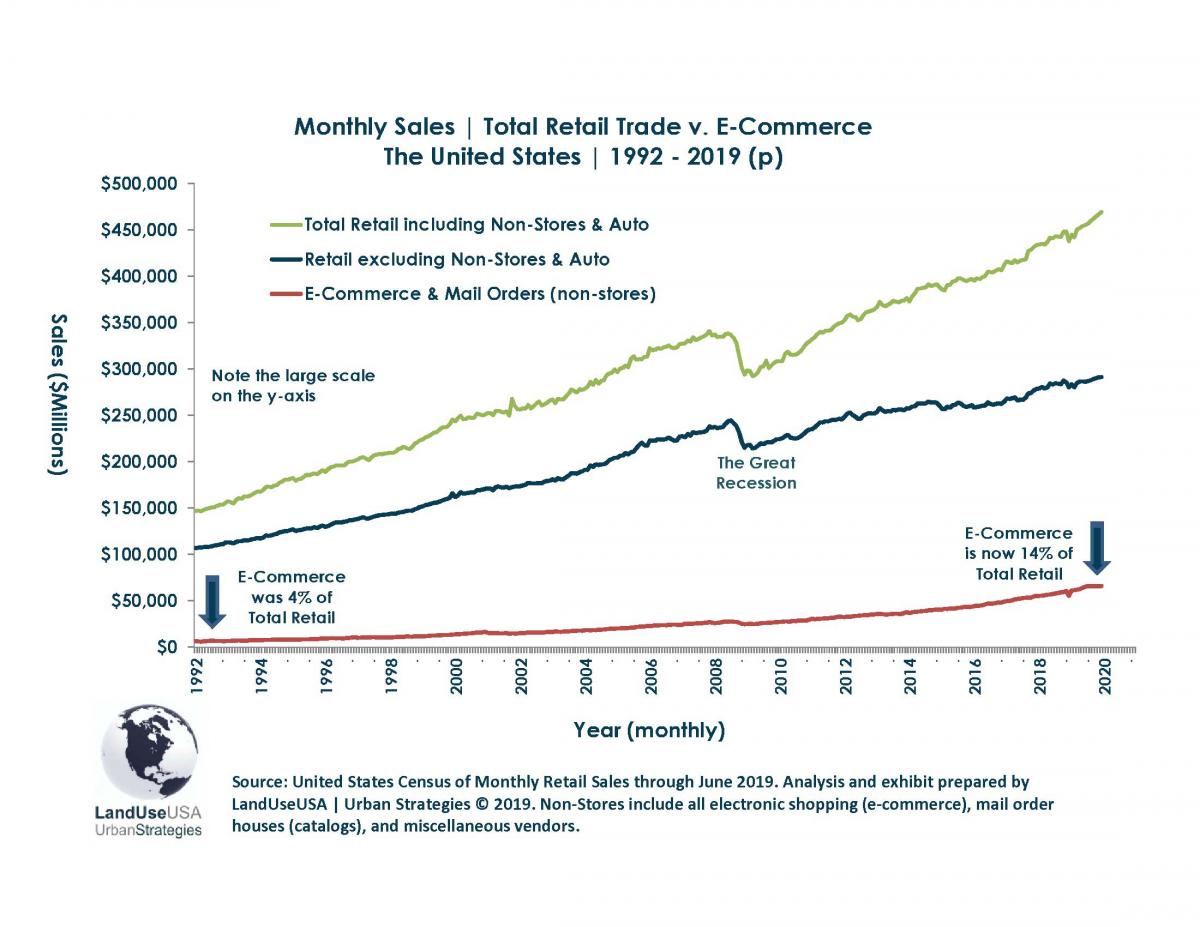

Increasing retail sales: A hypothetical Retail Apocalypse should also be supported by a decline in brick-n-mortar retail sales—but again that notion can be refuted with data. Figure 4 demonstrates that sales (given as monthly in Figures 4-7) for retailers are continuing to grow—this excludes non-stores, e-commerce, and automotive dealerships.

There appears to be more volatility since the Great Recession, and a minor dip occurred in the mid 2010s. However, sales have since rebounded and the long-term prospects look promising. (E-commerce, mail order houses, and other non-stores are also shown on Figure 2, and will be addressed in detail in a future article.)

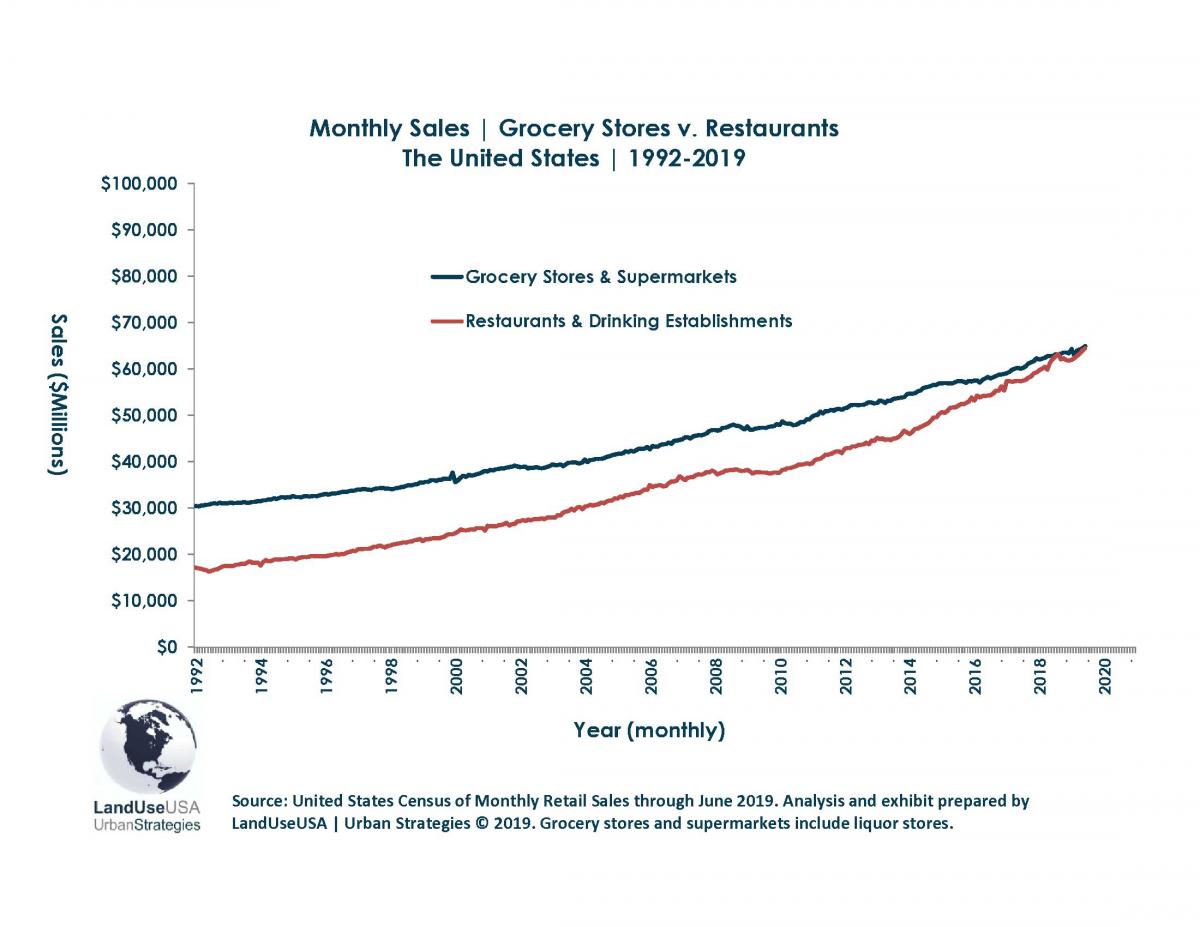

A closer study of retail subcategories points to some winners and losers. Grocery stores and supermarkets are experiencing the most robust growth in sales (see Figure 5). However, they will soon be passed up by revenues among restaurants and drinking establishments. Although restaurants are not technically included in the BLS classification of retail trade, they are important because they attract shoppers, enhance retail shopping experiences, and are good solutions for filling retail vacancies.

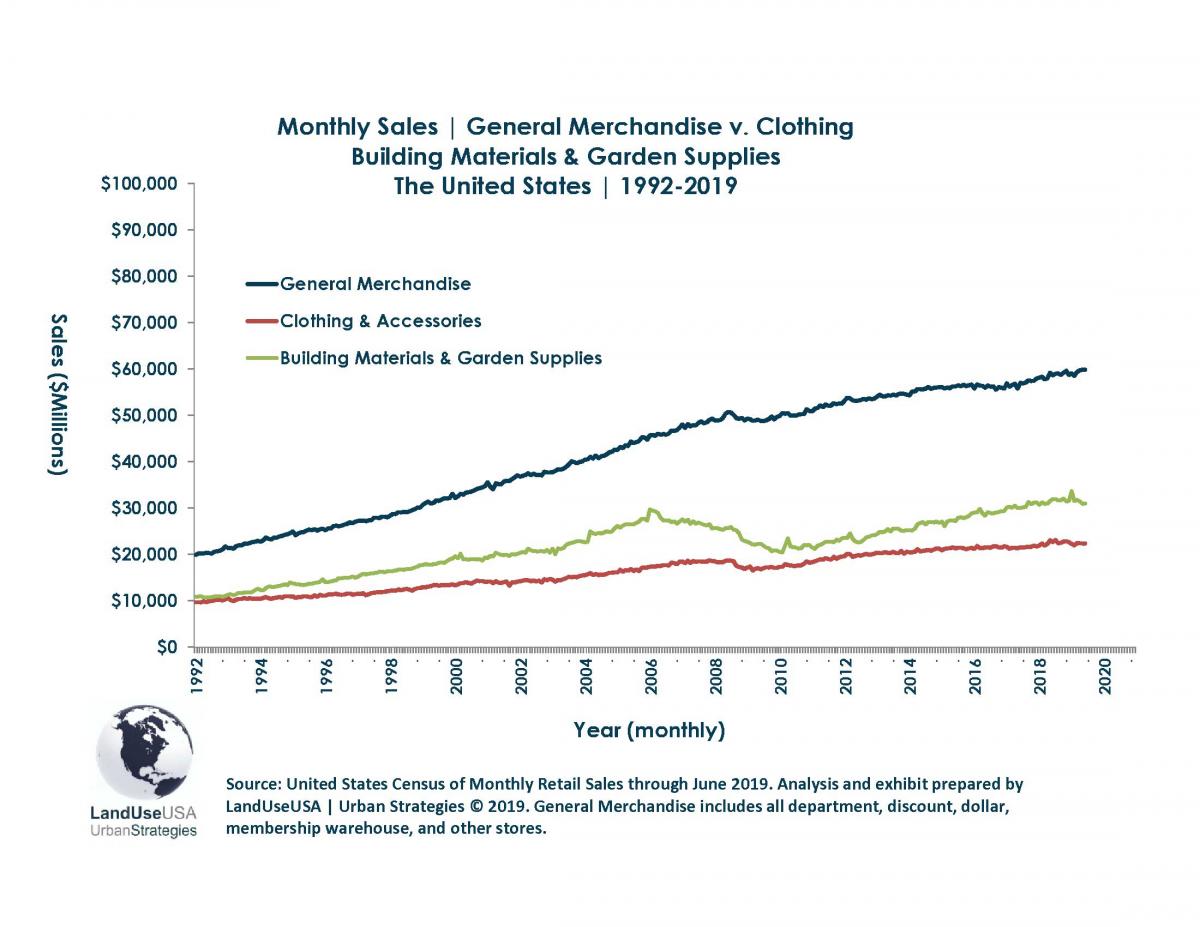

Figure 6 shows that other brick-n-mortar categories are benefiting from moderate yet steady growth in sales, including general merchandise, clothing and accessories, and building materials (including all hardware stores) and garden supplies. The general merchandise category covers all conventional department stores, including growing chains like Bon-Ton (re-opening stores), Nordstrom, and Dillard's. It also includes all growing chains and brands like Walmart, Target, Costco, Dollar General, and Five Below.

As an interesting side note, Walmart’s domestic sales represent about 45 percent of general merchandise revenues for the United States (source: Walmart 2019 Annual Report and the Census of Monthly Retail Sales).

The discount and dollar store categories have proven to be especially recession-proof. During the Great Recession, shoppers shifted their spending away from luxury brands and conventional department stores. Instead, they learned to value thrifty shopping and enjoyed the gratification of finding good bargains and deals. This shift in shopper attitudes has continued even through the economic recovery.

The clothing and accessories category includes apparel chains and tenants, but excludes department stores. Examples include growing brands like Old Navy, Ross Stores, Aerie (by American Eagle), Marshalls and T.J. Maxx, Burlington (Coat Factory), Nike/Foot Locker, Sierra Trading Post, and Dry Goods.

Building materials and hardware took a big hit during the Great Recession. The housing slump had home owners deferring maintenance and improvements while developers fled the industry and construction slowed to a halt. However, it has since recovered and has resumed positive trend of growth in sales. Growing brands in this category include names like Harbor Freight Tools and Tractor Supply Company.

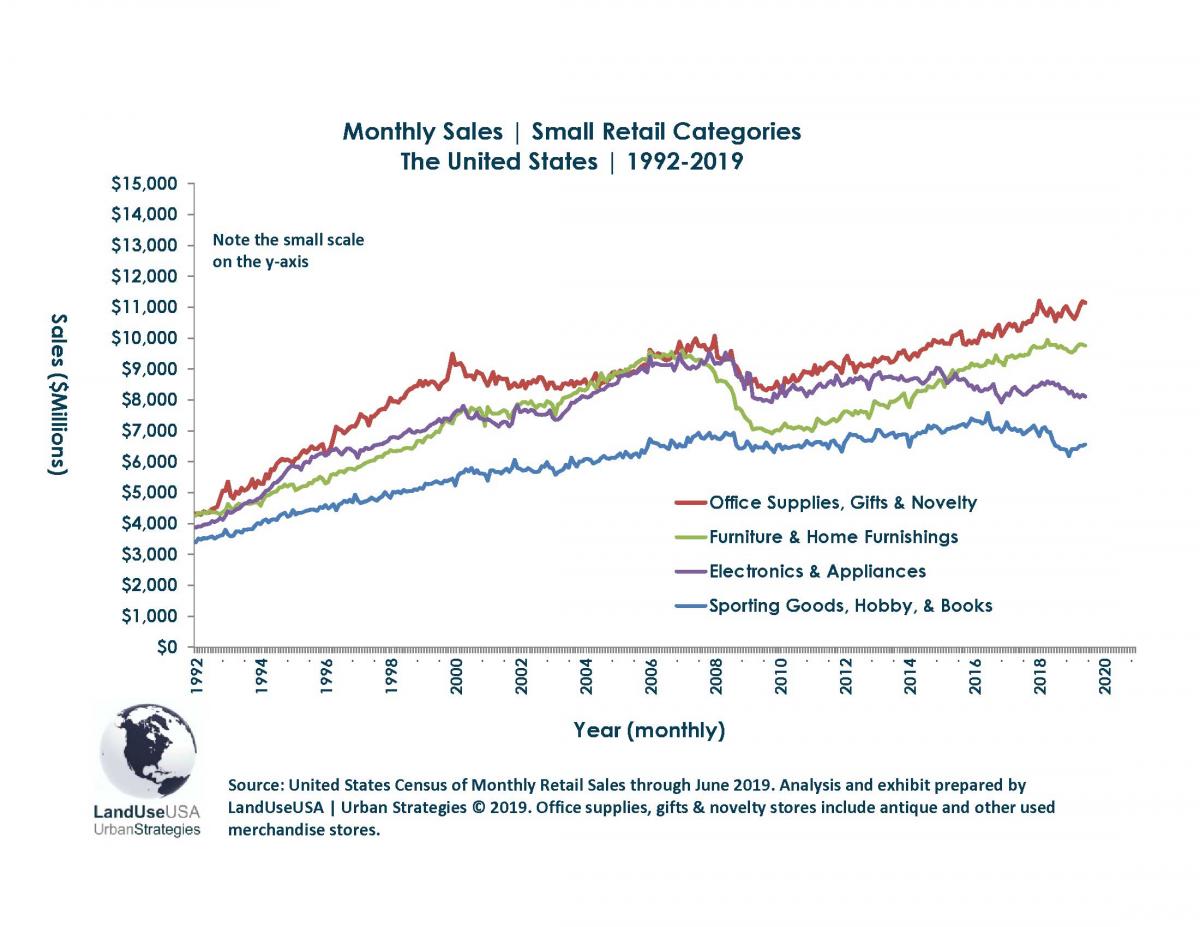

Figure 7 shows four smaller brick-n-mortar retail categories, with two winners and two losers. Office supplies, gifts, novelty stores (including antique stores), furniture, and home furnishings have thrived since the Great Recession. In comparison, sales in electronics, appliances, sporting goods, hobby supplies, and book stores have stalled and struggled in recent years.

These impacts are often attributed to the impact of e-commerce—and this is largely true. However, the impacted retail categories are relatively small compared to the growing categories. The two impacted categories collectively have monthly sales of less than $20 billion. In comparison, the growing categories (grocery stores, restaurants, general merchandise, clothing, building materials, furniture, and miscellaneous) collectively exceed $130 billion.

Steady occupancy rates: Retail analysts throughout the industry are reporting solid and steady retail occupancy rates among all retail space (sources: CoStar, Reis, ICSC, and NAR). Industry-wide occupancy rates are currently holding steady at 90-95 percent, with some variation depending on the methodology, type of shopping center, and submarket. The overarching consensus among analysts is that open air “town centers” have average occupancy rates of about 95 percent; whereas strip centers have average occupancy rates of 80-85 percent.

The most sobering news is that vacancy rates in regional malls have increased to 13 percent, from 10 percent, since 2013. Regional mall vacancy rates could climb to 15 percent by 2020 and following additional closures among conventional mall anchors and tenants.

Retrofits help occupancy rates: Anchor store closures (like Macy’s, Lord & Taylor, JC Penney, and Sears) can have profound negative impacts on the marketability of regional shopping centers. Malls that lose their anchor stores will also struggle to retain smaller apparel tenants. When the anchors downsize or close, all of the tenants suffer.

The relatively high vacancy rates among regional malls and strip centers are expected to recover over time, aided by the demolition of obsolete structures and retrofits. Vacant big-boxes can also be converted or adapted into non-retail uses, including services that complement retail and improve the overall experience for shoppers and patrons.

Retail property owners are learning to be resilient and are becoming increasingly successful in luring a wide range of alternative uses for vacant anchor space. “Experiential” uses like entertainment and amusement arcades, health and wellness spas, fitness centers and gyms, event space, and work share offices are especially effective in attracting patrons. These patrons can be converted into shoppers who generate sales and support the retail tenants.

Retrofitting vacant space—examples of non-retail uses

- Entertainment and amusement arcades, childcare centers

- Health and wellness spas, fitness centers, gyms

- Event space with rooftop beer gardens, stages, mini-golf

- Work share, co-op work space, business accelerators and incubators

- Overnight accommodations, hotels, pet retreats

- Medical urgent care, labs, imaging, radiology, dialysis

- Technical training schools, computer training centers

- Marketing and call centers, phone orders, mail orders

- Urban housing formats like lofts, townhouses

Conclusion

The future for brick-and-mortar retail is far less bleak than the scene painted by mainstream media. Although e-commerce is taking a larger share of the pie, brick-n-mortar and physical store sales are also continuing to grow. Most of the chain store closures are limited to certain segments of retail—particularly department stores anchors and apparel tenants of sprawling regional malls and strip centers.

Changes in technology and consumer preferences are also transforming the retail industry. These changes include the downsizing or “right-sizing” (and sometimes the demise) of chain stores and brands that were overbuilt, outdated, and either unwilling or unable to keep up with emerging new trends, fashions, and shifts in shopper behavior. Fortunately, there is a new store, merchant, or restaurant that opens for every chain store that closes.

Brick-n-mortar retail is here to stay. For the foreseeable future, shoppers will continue visiting physical stores to enjoy the shopping experience for its entertainment value (“retail therapy”), for instant shopping gratification without delivery delays, to touch and test merchandise, and to leverage omni-channel strategies like click-and-collect and fee-free returns. Merchants and independent proprietors who can leverage the newest trends will also be the most likely to succeed.